Home Inspection

Why You Need a Home Inspection

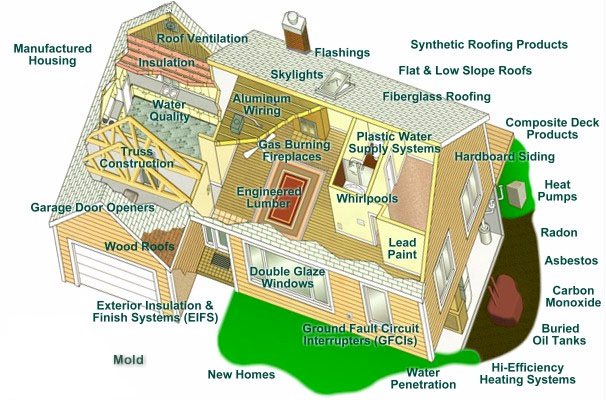

Home inspections give you, the buyer, detailed information on potential problems--information you need to make a wise decision. In a home inspection, a qualified inspector takes an in-depth, unbiased look at your potential new home to:

- Evaluate the physical condition: structure, construction, and mechanical systems

- Identify items that must be repaired or replaced

- Estimate the remaining useful life of the major systems, equipment, structure, and finishes

The home inspection does not evaluate the value of the house. That’s what an appraisal does.

Getting a Home Inspection

The first step is to call a qualified home inspector, someone who is very experienced evaluating:

- Home construction

- Proper installation of construction materials

- Maintenance

A qualified home inspector has performed hundreds of home inspections and knows the job.

Finding a Qualified Home Inspector

To find a qualified home inspector, try these sources

Professional organizations. Some states have professional organizations that require home inspectors to pass tests and meet minimum qualifications before becoming a member.

Yellow Pages. Look under "Building Inspection Service" or "Home Inspection Service"

The Bottom Line: Spending Hundreds May Save Thousands

A home inspection is a good investment to help you make the biggest investment of your life. Before you sign the contract, make sure you know the physical condition of your home in order to make a wise decision.

Most Frequently Asked Questions and Answers

1. Why do I need a home inspection? Aren’t the physical deficiencies noted in the appraisal?

Appraisals are prepared for lenders; home inspections are for you, the buyer. Home inspections give the buyer detailed information on the physical condition of your home.

2. Who pays for the home inspection?

You, the home buyer, pay for the inspection. Most home inspections cost between $200 and $300.

3. Will a home inspection hurt my chances of getting a mortgage?

No. The home inspection is only for you, the buyer. Therefore, it will not impact your chances of getting a mortgage. Many mortgage lenders encourage home inspections.

4. Does HUD recommend certain home inspections?

No. It is the buyer’s responsibility to obtain and carefully review a qualified inspector.

5. Am I entitled to a copy of the home inspection report?

Yes, the report will be prepared for you

6. If the inspection identified major deficiencies, who pays to have them repaired?

The cost to repair major deficiencies is typically negotiated between the buyer and seller.

7. Could my application for a HUD-insured mortgage be rejected because of the home inspection report?

No, unless the mortgage company required a home inspection, and the problems are significant.

8. Does HUD require a home inspection report?

No, but HUD strongly recommends that you get a home inspection report before settlement.

9. How long does it take for a home inspection report to be prepared?

Usually, it takes five to seven days, but this is negotiable.

10. If the home inspection finds repairs that are not noted on the appraisal, would I have to borrow more?

No, the appraisal assumes that all required repairs are completed. Any additional repairs noted by the inspector will not impact the appraised value.

11. If my home inspection reports major deficiencies, can my contract be cancelled?

For the contract to be cancelled, your agreement of sale must state that the contract may be cancelled if the repairs indicated by the home inspection exceed a certain dollar amount. Before you sign the agreement for sale, ask your Realtor or attorney to make sure you have this protection.